Democrats caving on health care is worse than you think

Polygraph | Newsletter n°323 | 24 Nov 2025

IN THIS NEWSLETTER: After pushing millions from Medicaid into the ACA Marketplace under Biden, Democrats just walked away from the subsidies that kept Marketplace coverage affordable.

*My latest in Popular Information: How Trump’s trillion-dollar war machine enriches the 1% Please read and share with your representative and senators.

*Thank you, Alissa Q., for becoming Polygraph’s latest VIP member! Please consider joining Alissa and the others thanked at the bottom of each note to support my work:

Situation

The issue at the heart of the recent government shutdown was health insurance subsidies, specifically, enhanced subsidies for the Affordable Care Act (ACA) Marketplace. They originated in the 2021 American Rescue Plan, were extended by the 2022 Inflation Reduction Act, and will expire at the end of this year if they aren’t extended again.

Democrats had refused to vote on any budget deal to reopen the government without funding for enhanced subsidies until eight Democratic senators (Cortez Mastro, Durbin, Fetterman, Hassan, Kaine, King, Rosen, Shaheen) joined Republicans to advance a funding bill that excluded them, clearing the way for the bill’s enactment. The eight Democrats say they secured from Republicans a future vote on Marketplace subsidies — that is, they made a pinky promise with the party that nearly repealed the entire ACA a few years ago. They’re also touting “wins” such as backpay for federal employees and resumed SNAP funding, but those are issues related to the shutdown itself, neither of which was a partisan sticking point.

Democrats could have tied the shutdown to any number of demands, but decided on Marketplace subsidies, launching a whole ad campaign around it. That Democrats came away from the highly publicized and self-promoted standoff with nothing has prompted some lawmakers and several major progressive organizations to call on Chuck Schumer (D-NY), the historically unpopular Senate Majority Leader and currently the highest-ranking Democrat in office, to resign.1

What happens if the Marketplace subsidies expire? Enrollment in the Marketplace is 24.3 million. Most, if not all, will face higher monthly health insurance premiums in January, for two reasons.

First, Marketplace insurance companies have decided to increase their premiums by 26% next year.2 This is in keeping with the trend of private health insurance costs growing considerably faster per enrollee than Medicare or Medicaid.

Second, nine in ten people with Marketplace coverage have health insurance plans subsidized by the government. The enhanced subsidies expire at the end of December.

An expensive basic necessity is getting even more expensive, and a policy that helps people afford it is being taken away. This type of double whammy has become something of a theme, hasn’t it?

Background on the ACA Marketplace subsidies

Feel free to skip this part.

Because the US health insurance system is so fragmented, there are major coverage gaps. One is the bloc of 40–50 million people who don’t get health insurance from their jobs, are too young to qualify for Medicare, and earn too much to qualify for Medicaid. There are several obvious solutions to this problem — lower the age threshold for Medicare, raise the income threshold for Medicaid, eliminate thresholds for either/both, etc. What we got instead was the ACA Marketplace. It’s expensive for both the government and health insurance “consumers.”

In addition to the operating and administrative costs of the Marketplace, the US government also spends quite a lot subsidizing private health insurance companies’ premiums. Federal support for the Marketplace totaled $125 billion in 2024. Extending the enhanced subsidies alone is projected to be $35 billion annually, on average — though that estimate is probably too low, because it was made before Marketplace insurers decided to raise their premiums by 26% next year.3 Per enrollee, Marketplace coverage is far more expensive than Medicaid.

Immense federal subsidies notwithstanding, Marketplace coverage is still quite expensive for health insurance “consumers” ($500 per month/$6,000 per year for one of the cheaper individual plans). There are over 27 million uninsured Americans, and about two-thirds say their lack of coverage is due to the high cost of health insurance.

Democrats caving on health care is worse than you think

The looming expiration of Marketplace subsidies doesn’t help Republicans, but it’s likely more politically damaging to Democrats.

The bulk of the media critique has focused on the pattern of Democrats failing to stand up to Trump, thereby alienating their base. As a result, you’ve likely recently heard critics describe the Democratic Party as “feckless,” “cowardly,” “weak,” “if irritable bowel syndrome were a political party,” and so on.

A related but more important pattern is the Democratic Party’s alienation of working-class voters. Democrats reneging on their no enhanced subsidies, no budget deal ultimatum isn’t just bad optics — it betrays the lower-income people the previous Democratic administration funneled from Medicaid to the Marketplace, promising affordable coverage.

1. Historic Marketplace enrollment, historic Medicaid disenrollment

Biden campaigned on record-level growth in Marketplace enrollment during his abbreviated 2024 reelection bid and listed it as one of his top healthcare achievements near the end of his term. In January 2025, the Biden administration announced that it set “another all-time record” for Marketplace sign-ups. Biden himself boasted that “nearly 24 million Americans have signed up for Affordable Care Act coverage. That means that enrollment has nearly doubled since I took office. That’s no coincidence.”

Biden actually sold himself short there — Marketplace enrollment for 2025 ended up at 24.3 million, more than double the number he inherited in 2021:4

2018: 11.8 million

2019: 11.4 million

2020: 11.4 million

2021: 12.0 million

2022: 14.5 million (+2.5M)

2023: 16.4 million (+1.9M)

2024: 21.4 million (+5.0M)

2025: 24.3 million (+2.9M)

The historic growth in Marketplace enrollment under Biden was made possible by two main factors.

First, the enhanced Marketplace subsidies that made private coverage less expensive, enacted as part of the March 2021 American Rescue Plan. After Marketplace enrollment had basically flatlined after 2015, the introduction of the enhanced subsidies prompted the 2.5 million-enrollee jump from 2021 to 2022 and the smaller but still sizable 1.9 million increase from 2022 to 2023.

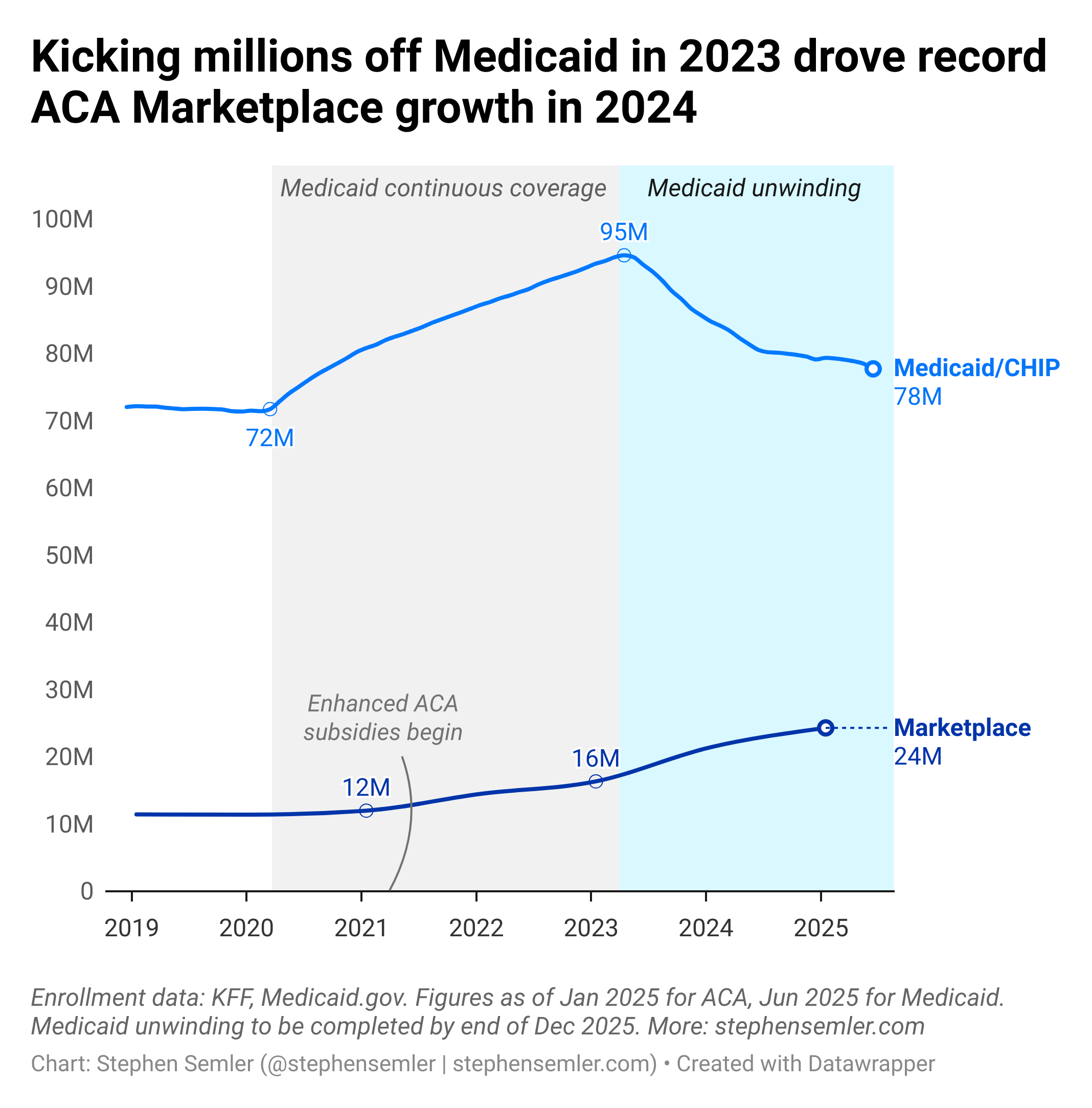

Second, the Medicaid “unwinding.” That the largest enrollment jump in the Marketplace occurred from 2023 to 2024 (and second-largest from 2024 to 2025) isn’t a coincidence. As the chart below shows, the record increase in Marketplace signups in 2024 is mostly attributable to the Medicaid purge that began in 2023. From April 2023 to September 2024, 26.8 million people lost Medicaid coverage.5

The Medicaid unwinding was the largest nationwide healthcare coverage transition since the Affordable Care Act itself. Still, some people write off over 25 million losing health coverage because Medicaid enrollment shot up from March 2020 to March 2023.

In early 2020, Congress wisely sought to avoid lower-income Americans being kicked off health insurance during a public health crisis. In March 2020, Congress passed the Families First Coronavirus Response Act, which required states to maintain enrollment of nearly all those on Medicaid in exchange for an increase in federal funding to accommodate the larger enrollment (see Sec. 6008). This became known as the “continuous enrollment” or “continuous coverage” condition.6 This condition would be active so long as the COVID-19 Public Health Emergency (first declared on January 31, 2020, and renewed by the acting administration many times thereafter) remained in effect.7

Because Medicaid was still taking on new participants, enrollment grew from 72 million in March 2020 to 95 million three years later. By March 2023, more than one in four Americans were covered by Medicaid, including half of all children.8

Continuous coverage was excellent from a public health perspective. For example, one study found that

“Medicaid beneficiaries experienced a decline in coverage interruptions in 2021 and 2022 relative to privately insured individuals…with less reporting of unaffordable healthcare needs and delayed medical care due to cost…The continuous Medicaid coverage provision…was associated with enhanced coverage stability and improved access to care.”

The Medicaid unwinding process — which was an administrative disaster — had the opposite effect on public health. For example, one study in the Journal of Addiction Medicine found that unwinding was linked to

“A rise in the number of people ending medication treatment for opioid use disorder, as well as a decrease in the number of people beginning such treatment…changes were greatest in states that have had the largest disenrollments.”

Florida disenrolled more than 400,000 people from Medicaid in the first three months after unwinding began. Texas disenrolled over 500,000 people in a single month, the vast majority for not submitting the proper paperwork. Two-thirds of the 26.8 million people kicked off Medicaid nationwide as of September 2024 were disenrolled for procedural or administrative reasons, meaning they lost coverage because of red tape or the state dropped them in error, not because they were officially determined to be ineligible.

People are still losing their health insurance as part of the Medicaid unwinding — states have until the end of December 2025 to complete eligibility redeterminations.

^Alt text for screen readers: Kicking millions off Medicaid in 2023 drove record ACA Marketplace growth in 2024. This line chart shows the growth in Medicaid and CHIP enrollees under continuous coverage — from 72 million to 95 million — and the decline under unwinding, from 95 million to 78 million. It also shows that Marketplace enrollment grew from 12 million to 16 million after enhanced subsidies started in March 2021, and from 16 million to 24 million as millions were kicked off Medicaid. Enrollment data: KFF, Medicaid.gov. Figures as of January 2025 for Marketplace, June 2025 for Medicaid. Unwinding to be completed by the end of December 2025.

2. A politically engineered Medicaid mass displacement

Nearly ten months after the Medicaid purge started, a Biden administration press release titled “Record Marketplace Coverage in 2024: A Banner Year for Coverage” announced that

“We are now seeing something closer to the full effect of the Biden Administration’s policies to strengthen Marketplace coverage options, which previously had been partially masked by unusually high Medicaid enrollment due to the COVID-era continuous coverage provisions.”

As that quote suggests, the Biden administration’s intent was to push people from Medicaid into the Marketplace. It made sure that happened by: 1) extending Marketplace subsidies through the Inflation Reduction Act in August 2022, 2) signing off on Medicaid unwinding in December 2022, and 3) channeling those disenrolled from Medicaid into the Marketplace after unwinding began in April 2023.

I understand that attributing blame to Biden for mass Medicaid disenrollments is considered controversial, but it really shouldn’t be. These are facts:

Medicaid continuous coverage was linked to the COVID-19 Public Health Emergency — coverage would remain in effect so long as the emergency declaration did, which the administration can (and did) repeatedly renew.

Medicaid continuous coverage did not require funding from Congress — it was funded by formula-driven mandatory spending (not congressionally-approved discretionary spending).

The President could end Medicaid continuous coverage by a) signing a bill delinking continuous coverage from the Public Health Emergency, or b) declaring an end to the Public Health Emergency. Biden did both.

Biden’s budget for 2023 — enacted through the Consolidated Appropriations Act, 2023 — delinked Medicaid continuous coverage from the Public Health Emergency, and set April 1, 2023, as the start date for gradually defunding continuous coverage and allowing states to resume disenrollments (see Div. FF, Title V, Sec. 5131). After urging its “swift passage,” Biden signed the legislation into law on December 29, 2022, as the last spending bill enacted by the Democratic trifecta. All but one Democrat voted for it.9

Had the bill not included that provision, Biden would have triggered Medicaid unwinding anyway after ending the COVID-19 Public Health Emergency on May 11, 2023.

A common defense of Biden’s behavior from Democratic partisans is that Medicaid continuous coverage originated as a temporary provision, so it should be temporary. That’s precisely the same argument Republicans are making now in opposing the extension of the enhanced ACA subsidies:

Democrats (2023–24): Medicaid continuous coverage originated among many temporary emergency measures authorized by legislation passed between March 2020 and March 2021 in response to COVID-19. The Medicaid unwinding was just a return to the status quo ante. In fact, more people are enrolled in Medicaid now than before the pandemic!

Republicans (2025): The ACA Marketplace enhanced subsidies were one of many temporary provisions enacted through the 2021 American Rescue Plan and other emergency legislation. The expiration of the subsidies is just a return to the status quo ante. In fact, despite the projected drop in Marketplace coverage, enrollment will still be higher than it was before the pandemic!

3. Migration to the Marketplace

In January 2023, the Biden administration created a Special Enrollment Period for people losing Medicaid to sign up for Marketplace coverage without waiting for the typical open enrollment period. It was scheduled to begin March 31, 2023 — the day before Medicaid unwinding began. Predictably, there was massive and highly unusual mid-year growth in Marketplace signups. Per KFF:

“Unlike most previous years, the individual market grew mid-year in 2023, outside the open enrollment window and at a time when attrition normally occurs. From early April to the end of September 2023, enrollment in the individual market grew by 5.7%, or just over 1 million enrollees.”

In March 2024, Biden extended the Special Enrollment Period to accommodate the spiraling number of Medicaid disenrollments. Per Politico:

“The move aims to minimize the number of people losing health insurance coverage in the run-up to the November election as a result of a nationwide purge of state Medicaid rolls…a process that’s resulted in the biggest reshuffling of the health insurance landscape since the passage of Obamacare itself.”

Biden administration officials worked to transition those who lost Medicaid coverage to the Marketplace. However, Marketplace enrollments didn’t appear to offset the effect of Medicaid unwinding, at least on children. Over 5.5 million kids lost public health insurance coverage from April to September 2023 alone. The uninsured rate among children in 2024 was higher than any year since at least 2017:

2017, 5.0%

2018, 5.5%

2019, 5.2%

2020, 5.6%

2021, 5.0%

2022, 5.4%

2023, 5.8%

2024, 6.1%

By June 2024, at least 3.5 million predominantly lower-income people kicked off Medicaid had enrolled in the Marketplace. As the Biden administration announced in 2024:

“Nearly 4.2 million more individuals with household incomes under 250% of the federal poverty level enrolled in [Marketplace] coverage compared to last year. This further indicates that lower-income individuals and families have enrolled…as states continue their post-COVID redeterminations of Medicaid.”

Lower income people made up the majority of the growth in the Marketplace enrollment under Biden: For example, 83% of the enrollment growth in the ACA Marketplaces from 2020 to 2024 was attributable to those with incomes below 2.5 times the federal poverty level.

Millions of them will lose coverage due to cost if there isn’t an extension of the enhanced Marketplace subsidies — the subsidies Democrats just caved on in the shutdown standoff. Many of these enrollees have Marketplace coverage in the first place because they were kicked off Medicaid by a bill enacted under a Democratic President, House, and Senate. What message are Democrats sending to the working class?

SPECIAL THANKS TO: Abe B., Alan F., Alissa Q., Amin, Andrew R., AT., B. Kelly, BartB., BeepBoop, Ben, Ben C.,* Bill S., Bob N., Brett S., Byron D., Carol V., Chris, Chris G., Cole H., D. Kepler, Daniel M., Dave, David J., David S.,* David V.,* David M., Elizabeth R., Errol S., Foundart, Francis M., Frank R., Gary W., Gladwyn S., Graham P., Griffin R., Hunter S., IBL, Irene B., Isaac, Isaac L., Jacob, James G., James H., James N., Jamie LR., Jcowens, Jeff, Jennifer, Jennifer J., Jessica S., Jerry S., Joe R., John, John, John A., John K., John M., Jonathan S., Joseph B., Joshua R., Julia G., Julian L., Katrina H., Keith B., Kheng L., Lea S., Leah A., Leila CL., Lenore B., Linda B., Linda H., Lindsay, Lindsay S.,* Lora L., Mapraputa, Marie R., Mark L., Mark G., Marvin B., Mary Z., Marty, Matthew H.,* Megan., Melanie B., Michael S., Mitchell P., Nick B., Noah K., Norbert H., Omar A., Omar D.,* Peter M., Phil, Philip L., Ron C., Rosemary K., Sari G., Scarlet, Scott H., Silversurfer, Soh, Springseep, Stan C., TBE, Teddie G., Theresa A., Themadking, Tim C., Timbuk T., Tony L., Tony T., Tyler M., Victor S., Wayne H., William P.

* = founding member

-Stephen (Follow me on Instagram, Twitter, and Bluesky)

To be fair to Schumer, representing Democratic voters isn’t his job. “My job,” Schumer told the New York Times in March, “is to keep the left pro-Israel.”

You see, that’s the magic of the marketplace: if you make companies compete, that will keep prices from spiraling out…oh. Oh dear.

KFF: “Because the ACA’s tax credit is tied to the cost of the second-lowest cost silver plan, when these benchmark premiums rise, so does the federal cost of offering tax credits.”

Marketplace enrollment figures are tallied in January of each year, so 2021 enrollment is attributable to policy under Trump and 2025 to Biden. Medicaid enrollment, meanwhile, fell by 1.5 million under Biden.

The federal funding largely relieved states of budgetary pressure to accommodate continuous Medicaid coverage. Per Pew: In 2023, “states spent 15.1% of every state-generated dollar on Medicaid, up 2.2 percentage points from the previous year, though still about half a cent less than the 15-year average.”

If you were enrolled in Medicaid as of March 2020, state governments kept you insured and largely left you alone — no means-testing, no form-filling, etc. If your income went above the Medicaid threshold, you were spared from having to shop for insurance — which is terrifying and boring — and buy insurance, which is expensive. If you eventually got employer-covered insurance, you weren’t fearful of losing your health insurance if you lost your job, and you also didn’t feel bound to keep that job if you disliked or didn’t excel at it because you couldn’t otherwise afford health insurance.

As many others do, I use “Medicaid” to include the specific Medicaid government program and other programs for low-income individuals administered by the states, such as the Children’s Health Insurance Program (CHIP) and Basic Health Programs.

The one Democrat who rightfully voted against the 2023 omnibus bill: Rep. Ocasio-Cortez.